Natural gas was heavily bid in April, after falling to $1.84 in late March. Today's close at $2.06 is still within the coal-switching price range, though the forward curve is in steep contango, rising to about $2.70 for the November contract.

There seems to be excitement around two major price drivers: (1) plateau/decline in domestic production, and (2) the march toward LNG exports, which have commenced and are running about 0.5 to 0.6 BCFD at present. However, unless we soon see a notable decrease in production from current levels, the hope for further increases will have to come from weather and economic recovery. The US economy is growing too slowly to generate the kind of power demand growth we have seen in earlier recoveries, and many ISOs are forecasting 1% or lower annual demand growth.

I would contend that the power generation market has the potential to disappoint gas bulls. Acknowledging that there will be further gains from coal plant closures, the fact remains that coal switching is the source of so much current demand that a return to the $3 price range for Henry Hub would quickly offset that.

The other problem, and it is a big one, is the rise of renewables. We are in an environment where power demand growth is hard to detect. And total US daily demand averages somewhere near 11,000 GWH:

If power demand is growing nationally at 0-1%, that's an increase of between zero and 110 GWHD. With that in mind, the expected new installs of solar and wind this year, adjusted for their anticipated capacity factors, only need to exceed that number in order for the hydrocarbon-based power market to shrink. Here are the monthly historicals for those two power sources:

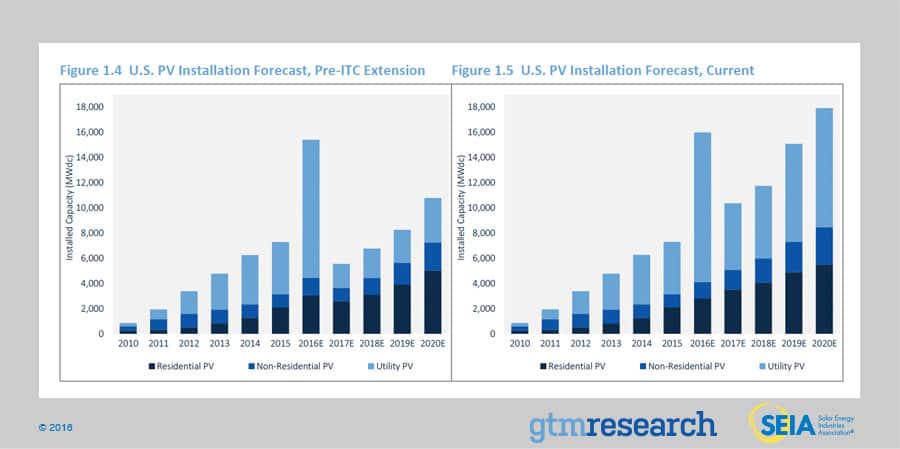

Solar power alone, the runt of the renewable litter, is slated to see 16 GW of new capacity in '16 (including distributed power and utility scale). If that had a 30% capacity factor, it would mean a 115 GWHD increase in generation! And solar is just a shadow of wind (heh, sorry, who can resist cheap irony?). Texas alone will install 8 GW of wind in 2016, and that has historically been at a 35% cap fac. So there is no room at the inn for carbon-based generation growth, unless we see economic growth, or a migration to electric cars, on a scale that nobody is forecasting at this time.

Can gas go to $3? Absolutely. But barring persistent abnormal weather, the glass ceiling is at $3 or below. The 2 year decline in rig count has some licking their chops over production declines, but the uncompleted well inventory and the drilling efficiency of the few working rigs will address any shortfalls. And at $3, there are enough economic drill sites that we should see a rapid return of the rig fleet, albeit at much lower drilling and fracking day rates.