Shale gas math has proven hard for producers, consumers, and investors to accept. Resource scarcity was the reigning paradigm, and the rules were:

- Hydrocarbons getting harder to find

- Each well costs more (inflation, deeper/remote drilling)

- Each well finds less (infill drilling, downspacing, weaker prospects, depleted fields)

The shale revolution came, but it didn't seem sufficient to offset production declines because:

- Decline rates were high

- Prospects were few (for a long time just the Barnett and Fayetteville)

- Wells were expensive

But production grew, and grew. New reserves were found onshore. Technology advanced, costs came down. So gas prices came down to the point that demand was elastic by competing with coal.

But whether it is the human tendency to anchor on the status quo, or to doubt revolutionary claims, or something else, the situation is setting up again for natural gas. Old metrics die hard, and the legacy cost structures and productivity seem to be blinding us to the (increasingly) obvious.

Exhibit A: Shale basins and rig productivity, from Baker Hughes Q2 2013:

Consider the best known basins now, the Marcellus and Utica. 608 wells were drilled in these two plays in Q2, and rigs were averaging a little less than 2 wells per month, so an average of 113 rigs were working, about 30% of the gas rig fleet.

What is the average well going to produce? This is an important question. The Utica is perhaps a little early to set a type curve on, with about 500 wells drilled and only about 125 producing. But the early wells are also typically improved upon over time, and the best wells to date were drilled by Antero Resources, delivering what are frankly mind-boggling flow rates, around 8-10,000 BOE per day, much better than the best Marcellus wells.

On the Marcellus side, there are 3 or 4 well types at this point:

- Dry Northeast

- Dry Southwest

- Rich Southwest

- Super-Rich Southwest

These wells are generating 4 -15 BCF reserve estimates per well (dry gas only). The drilling is moving to the wetter regions, but still plenty of dry gas wells being drilled, and obviously the ability to migrate rigs quickly should gas prices perk up.

Here then is the basic truth:

200 wells per month, at 5 BCF dry gas reserve estimates = 1 Trillion cubic feet developed per month. At that constant development rate, production would peak at over 30 BCFD, multiples of what is being produced now. And wells are going down faster, cheaper, and finding more gas as these plays develop and operators improve completion techniques.

There is also a lot of undeveloped acreage, so prime drilling locations will not deplete quickly.

We are using the best play as the example, granted. But the data is lagging, and operators are projecting better results going forward. There are so many other upside risks to this, including stacked pay: The Upper Devonian is above the Marcellus, and early results are looking great. This can multiply reserves very quickly, and take advantage of existing infrastructure.

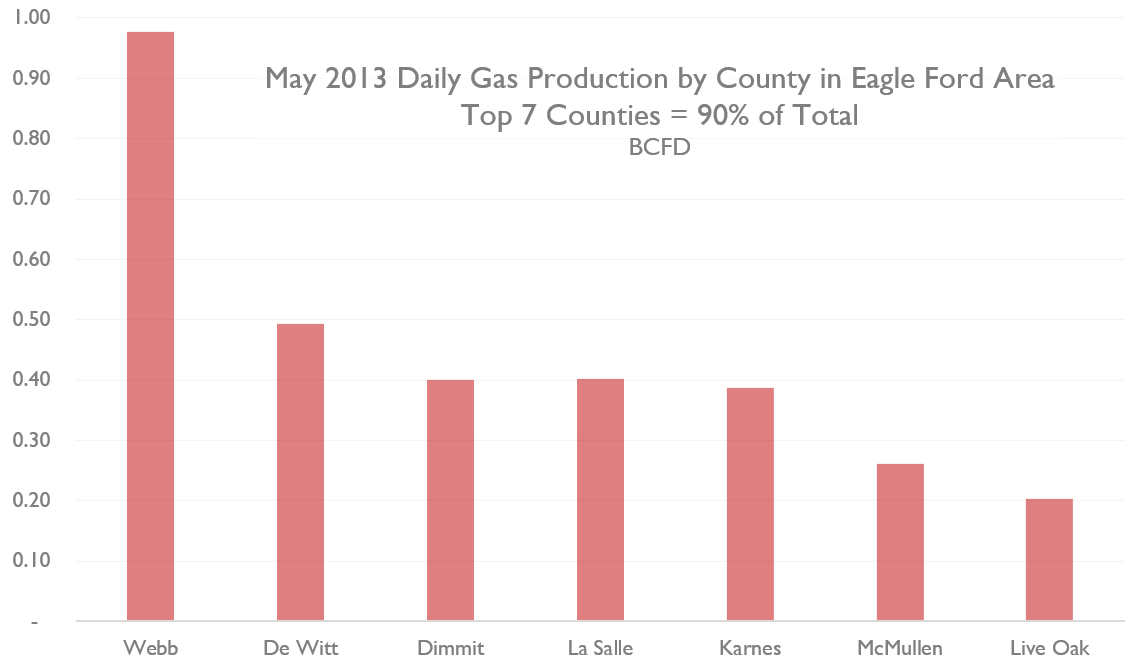

We could go through a similar exercise for the Eagle Ford, where drill times are much faster and the rig fleet is double that of the Marcellus/Utica (including oil rigs). The dry gas area of the Eagle Ford is being neglected now in favor of liquids to the north, but the reserves have been proved, and the locations are there when prices justify it and bottlenecks are cleared.

What is going to happen? Gas demand will steadily and noticeably rise due to electricity generation, industrial use, and finally LNG export. But the many BCFs these sources will eventually consume will not overwhelm production capacity, even at very low prices. The dreams of $5 gas are very very far off. Another expected outcome is a reduction in price volatility based on low gas inventory. If anything, the volatility will come when demand evaporates (unseasonable weather for example), and there is nowhere to put the produced gas. A few of these events seem inevitable.