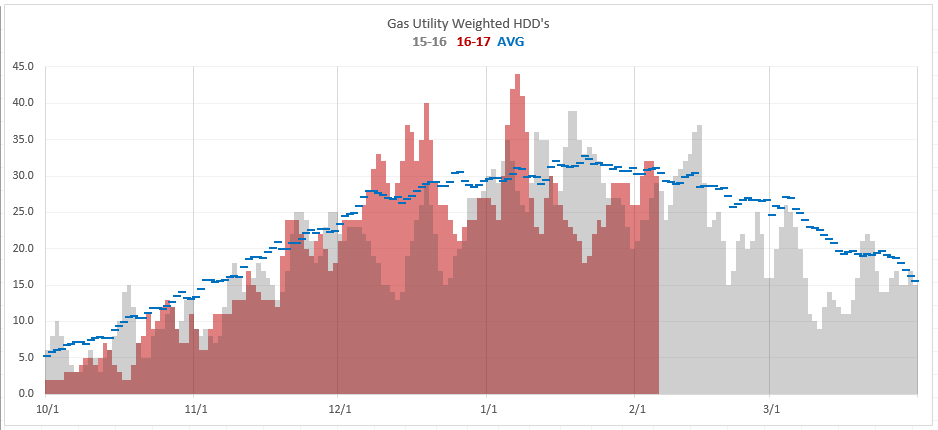

The big marketshare losses to coal this winter cast an ominous pall over the upcoming shoulder season demand for natural gas. A look at the MISO region this month tells a bit of the story, as we entered the month with high gas prices, which have begun to abate in the last few weeks.

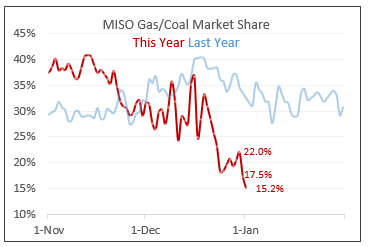

The grey line shows natural gas marketshare of thermal generation at various aggregate thermal demand levels in January 2016. It indicates that gas was able to maintain a 30%+ marketshare even at low burn levels.

This January (red line), lower thermal demand levels led to a steep drop in marketshare, going as low as 15%.

Isolating the most recent week (Jan 20-26) of this month shows marketshare slightly higher than the month as a whole, by perhaps 1-2%. That's probably statistically insignificant, but it points in the right direction, providing some hope that price sensitive generators are finding it more appealing to run gas turbines. Hopefully gas doesn't need to break below $3 to trigger further gains before shoulder season begins.

Here's another way of seeing the split between coal and gas in MISO, showing how much share gas lost since November: