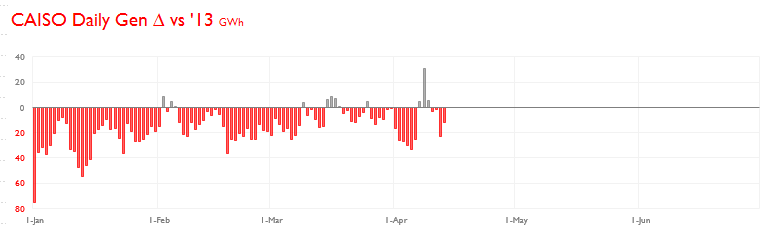

Solar continues its rapid expansion in California, both distributed and utility scale. The real impact of the incremental additions will be felt this summer, when daily generation peaks in the afternoon instead of after dark. In April, the peak is normally around 8 pm, so solar power is not shaving the peak.

Considering the average April daily load profile, here is the impact of utility scale solar additions in the last year. Again, this is how much more solar generation was added in the last year.

And here is the total current solar generation, as a component of average daily April load:

California should see a massive impact from solar energy expansion this summer. With over 100,000 rooftops now generating solar power on the other side of the meter (not reflected in the charts above), the total load should also see a reduction this summer on-peak. Estimates indicate that something like 800 MW of distributed solar are already operating in California, and growing.

This should accelerate the collision that appears inevitable between all the stakeholders of electric power, including the independent power providers. It is conceivable that total solar generation capacity could exceed 7 GW in California by next summer.

A compounding problem is the lack of power demand. Total electricity sales is in a noticeable decline in CA this year. The grid will be stressed, as will the balance sheets.