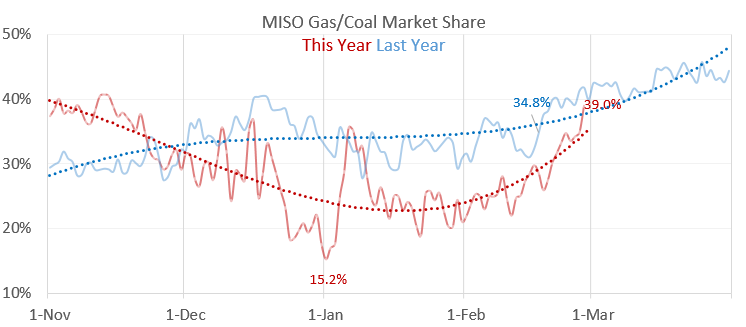

MISO Electric region has been quick to respond to changing gas prices, on the way up and now back down. Gas is quickly recovering the market share lost to coal since gas prices began rising in November:

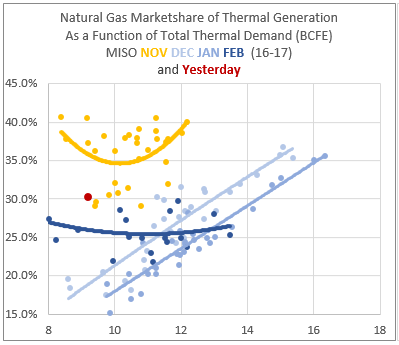

Yesterday's large increase in gas fired power generation set a big new high for the month of February, and put it on par with last February, despite current prices being 75 cents higher than last year.

This suggests that despite the weak weather, low aggregate power demand, and rise of renewables, and expected production bolus, it may be difficult to pierce a lower price boundary during the shoulder season. If $2.50 gas stimulates the same power burn demand as last year's sub $2 pricing, then it should be more than adequate to keep inventories in line.

We still have a few more weeks of weather influence before the mildness of late march limits cold spikes, so volatility can still prevail.