Visual exploration of US energy supply and demand

Wednesday, November 30, 2016

EIA Natural Gas Monthly Demand September 2016

Today's EIA Natural Gas Monthly contains few demand surprises, but it does confirm the step change in industrial demand, which was again roughly 1 BCFD above prior years.

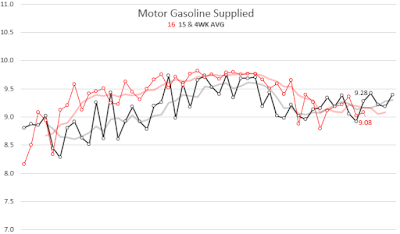

Motor Gasoline Demand Falls Below 2015

Today's EIA Report brought the 4 week average for motor gas demand below 2015, confirming the end of the gasoline growth story from the first half of the year.

EIA Electric Power Monthly

EIA Electric Power Monthly was released today, with data through September. It shows the gas coal market share basically flat with July and August, but shifting about 3% in favor of gas vs last September.

Tuesday, November 29, 2016

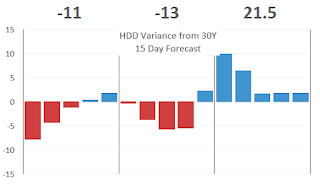

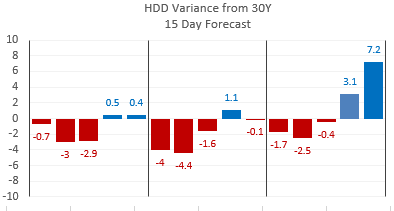

15 Day Weather Outlook

Gas is weaker this morning, as the out week forecast moderates a bit. The 11/29 12Z forecast shows net warmth in the 1-5 and 6-10 day, with a cool 11-15, for a net neutral HDD outlook.

MISO Gas to Coal Shift

Having previously noted the structural increase in natural gas fired power generation in MISO, the recent price spike in gas should reveal the component, if any, of the switch to gas that is price motivated.

Here is what the estimated daily burn (at a standard 800 heat rate) looks like for November, on a year-over-year basis. The timing of the Thanksgiving holiday will cloud the comparisons in the final week of the month, so this is a story that will unfold in the next few weeks if gas prices hold their ground.

Monday, November 28, 2016

Nuclear Power Output Drops Over Thanksgiving Holiday

A few reactors are down, which drove nuclear power output down to 92%, off about 2% from last week, and holding about 6% above this day last year.

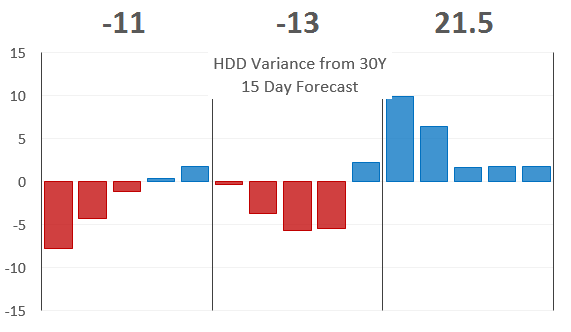

15 Day Weather Outlook: Severe Cold in Days 11-15

The volatile 11-15 period is indicating unseasonable severe cold, after 10 days of warmth.

Based on 11-28-16 12Z:

MISO Fuel Mix: Solid Coal to Gas Shift, But Low Demand

With November nearly complete, the year-on-year comparison of fuel mix and generation output shows gas stealing significant share from coal. The price environment for gas was similar in both years, and despite this gas took 4%+ market share from coal, as gas rose from 21% to 26%, and coal dropped from 49% to 45%.

Sunday, November 27, 2016

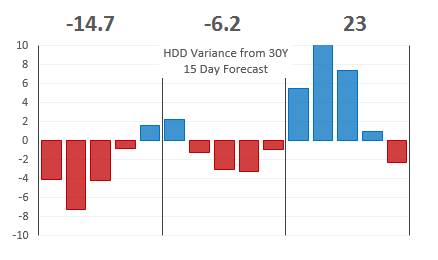

15 Day Weather Outlook

Nov 27 18Z weather shows unseasonable warmth in the near term, moderate middle period, then cold in the 11-15 day:

Western Hydro Generation in Last EIA Week

Hydro continued to run strong last week, but the excess generation in the Pacific Northwest moderated, when compared to last year.

In the BPA region, the Nov 19-25 average output was 8.8 GW, against last year's 7.5 GW.

In the BPA region, the Nov 19-25 average output was 8.8 GW, against last year's 7.5 GW.

Saturday, November 26, 2016

Warming 15 Day Forecast (15 HDD Below Normal)

15 day forecasts have been oscillating widely over the Thanksgiving holiday, with the current run dropping to -15 HDD, with a very warm start to the coming week. Should this verify, prices would come under pressure at the open. But 4 more GFS runs remain before that time.

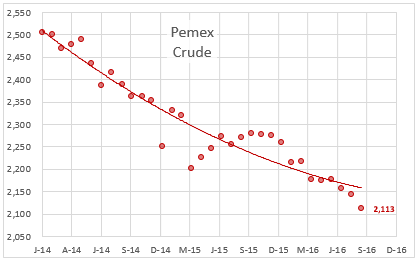

Pemex Reports Oil and Gas Production Declines to New Lows in October

Mexico's daily hydrocarbon output in October fell to new lows, with crude oil down 10,000 barrels per day to 2.103 million, and natural gas falling 0.036 BCFD to 5.583 BCFD.

The decline in gas output is consistent with increased imports of pipeline gas from the US, but crude exports did not fall in October, partly because domestic sales of motor fuel was substantially below last year.

Here are the details by the numbers:

Friday, November 25, 2016

Gas vs Coal Fuel Mix in MISO Power Generation

With comparably low natural gas prices year-on-year, MISO daily fuel mix reports show that natural gas has claimed a solid increase in market share over coal. Taking the daily reports, the percentage of carbon based power generation (ie gas+coal) claimed by natural gas is solidly above 2015. Thanksgiving falls earlier in '16, so we will see a drop in the mix 3 days earlier, but controlling for that we see a solid increase in gas market share at coal's expense.

Month to date, gas is claiming a 38% share this November, against a 30% share in Nov '15.

Thursday, November 24, 2016

Nuclear Power Generation Outlook

Nuclear power capacity factor has been exceeding 2015 throughout November, due to a lighter refueling schedule this season. That has resulted in the increasing displacement of natural gas fired power this year vs 2015 in November. This excess should begin to decline in 1 week, and vanish by December 22, which could generate more than 1 BCF in additional natural gas power demand in the Year-on-year comparison.

Wednesday, November 23, 2016

US Crude Production Rises Again, While Gasoline Demand Ebbs

The rig count is again proving a reliable predictor of lower 48 oil production, as this week's increase of 12,000 barrels per day reinforces a shallow upward trend since the bottom in August '16. Increased drilling activity, especially in the Permian Basin, and the encouraging initial production results, should amplify the production recovery in '17, barring a deterioration in prices.

Oil and Gas Rig Count Trends Continue Upward in Shortened Week

The shortened Thanksgiving week saw 3 oil rigs and 2 gas rigs added to the working fleet in the US, with a notable gain of +4 gas rigs in the Marcellus.

Weather Changes: Warm in the 1-10 Day, Cold Beyond

Today's 12Z run keeps a warm bias through day 13, then a couple days of sharp but very uncertain cold, for a net -9HDD from normal. That should add back quite a few BCF to storage estimates, but today's bullish storage report is holding sway for now.

Tuesday, November 22, 2016

Weather Forecast: Cold Outlook Moderates in 18Z Model Run

We lost about 17 HDDs over the last 12 hours, and the most recent (18Z) model run shows the 15 day outlook at about 4 HDDs less than normal, with the coldest period in the 10-14 day range.

Data available (slightly delayed) from a handy free site: Energy Metro Desk

Nuclear Power Output Exceeding 2015 by 1.4 BCFDE

With Wolf Creek #1 and Prairie Island #1 ramping up, nuclear power generation is running at 93.5% of capacity as of today, which is over 7 points higher than this day last year. This would represent roughly 1.4 BCF of natural gas replacement, if gas were the only fuel being displaced.

Natural Gas Demand Trends

Reviewing the EIA Natural Gas Monthly Demand Report, a few observations:

- Industrial Demand showed additional weather-adjusted demand in August, a long awaited source of incremental demand that should continue the uptrend.

- Despite similar levels of dry gas production to Aug of last year, Lease and Plant Fuel was below '15 by 0.09 BCFD, a reversal of a half year trend.

- Record electric power demand, which is already widely acknowledged. it was up 4.1 BCFD over Aug 2015.

- The curious decrease in richness seen in May-July was reversed, and BTU content rebounded by 3 BTUs/MCF.

Monday, November 21, 2016

EIA August Data Shows NGL Price Sensitivity

The August EIA Natural Gas Monthly Summary provides some confirmation of how much the 1H 2016 low natural gas prices drove the increase in liquids stripping from the gas stream. The gas price decline in late winter coincided with a sharp increase in NGL production as a % of gross natural gas withdrawals. Throughout 2014 and 2015, the percentage of gross withdrawals that were produced as liquids varied between 5% and 5.3%. Then when prices crashed in early '16, it rose steadily to 5.9%. Now, with the mid-summer recovery in prices, we see the first significant decline. From a 5.9% peak in June, the percentage fell steeply to 5.5% in August.

In a week, we should see confirmation of this trend if September numbers have fallen further still.

Heating Degree Day 5 Day Forecast Improves Slightly, Gas Prices Spiking on Longer Term Forecast

The weather outlook has improved for natural gas weighted utility demand, with the 5 day forecast approaching average, and the longer term (15 day forecast) at about +20HDD above average. Recent prices have strengthened enough to begin impacting coal to gas switching if it persists.

Sunday, November 20, 2016

Western Hydro Power Continues Outperforming

Bonneville Power Administration reports another leg up in hydro power generation this week, with another high set on Friday the 17th, at an average of 9.1 GW, nearly 2 GW above last year.

Saturday, November 19, 2016

Texas Solar Generation Begins to Contribute

Texas has built and/or permitted substantial solar capacity, and projected steady growth to 14GW by 2030. But that forecast has been continually revised higher, as solar costs have come down. Last year ended with around 250 MW of capacity, but new projects large and small have been coming on line lately, and daily generation is creeping upward.

The upcoming EIA week (Nov 11-17) will contain 14 GWH of solar generation, and that should grow each week. The impact on natural gas and coal generation will indeed be felt soon.

Friday, November 18, 2016

Rig Counts Revive: Oil Up +19, Gas +1

Rigs were put to work last week, with oil rigs adding 19 and gas another 1.

The rig count seems to be telling us something about where the economic opportunities are in this $45 oil, $3 gas market. The ten week chart shows significant gains in the Haynesville Shale, and the Permian Basin, with more recent, smaller increases in the Eagle Ford and Cana Woodford Shale. Not much change in either the Utica or the Marcellus.

But producers have added the most rigs in the last six weeks to the one basin that seems bottomless at any price.....

Nuclear Power Generation Massively Above 2015

In recent weeks, the reduced maintenance downtime of the US nuclear power reactor fleet has been offsetting natural gas demand at a level far above last year.

If the entire difference in nuclear generation output were replaced by natural gas fired power, it would yield about 7 BCF on last week's EIA natural gas inventory report, and for the current week (ending today), it would be closer to 12 BCF. That's a tremendous amount of offset demand. As winter gets underway and the capacity factors for both '15 and '16 approach 100%, this differential should diminish or reverse, which ought to significantly improve the supply/demand balance for natural gas.

Thursday, November 17, 2016

Weekly Natural Gas Storage Injection of +30 BCF Sets Record of 4,047

The EIA announced a 30 BCF injection for the week ended Nov 11, which brought storage up to record levels at 4,047 BCF. There were 7 more Gas-weighted heating degree days in the week vs 2015, and in general the offsets to power demand were greater this year, including increased hydro generation and nuclear output, so the gas supply fundamental picture is a bit tighter than the injection implies. And heating degree days were well below normal in both 2015 and 2016, to the extent that we would likely have seen a storage withdrawal under normal weather conditions. There should be about 17 more HDDs in next week's storage report.

Wednesday, November 16, 2016

ERCOT Set to Break Wind Generation and Penetration Records Tonight

ERCOT (Texas) projects the wind generation will exceed previous records for output, and penetration, tonight.

The Current All Time Record Values:

Output:

Record Wind Generation 14.023 GW

Record Wind Generation Time 02/18/2016 21:20

Penetration:

Record Wind Penetration 48.28 %

Record Wind Penetration Time 03/23/2016 01:10

ERCOT projects that the 14.023 GW record will be broken repeatedly tonight and tomorrow, with a 14.77 GW projected output during the 9pm hour tomorrow.

24 ERCOT Wind Generation Projections for 11-17016:

The Current All Time Record Values:

Output:

Record Wind Generation 14.023 GW

Record Wind Generation Time 02/18/2016 21:20

Penetration:

Record Wind Penetration 48.28 %

Record Wind Penetration Time 03/23/2016 01:10

ERCOT projects that the 14.023 GW record will be broken repeatedly tonight and tomorrow, with a 14.77 GW projected output during the 9pm hour tomorrow.

24 ERCOT Wind Generation Projections for 11-17016:

|

Based on projected system load, wind penetration should exceed 50% tomorrow morning during the 3 am hour, which would set a new record. It is important to note that installed wind capacity has risen about 2 GW since the previous records were set, so this achievement was all but inevitable.

Here is tomorrow's system load forecast, showing a 26.84 GW load at 3 am, which corresponds to a 14.26 GW wind forecast, for a penetration rate of 53.1%.

|

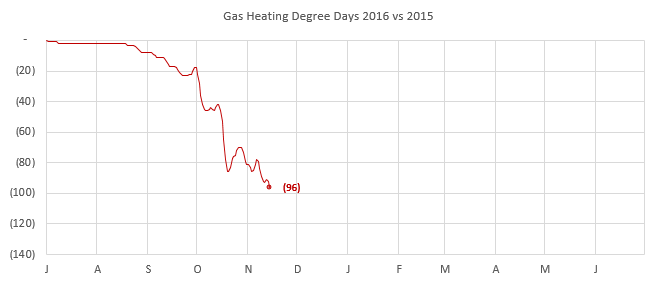

Comparison of Winter Heating Demand with 2015

Last year was warm, with a warm start. 2015 ended without about 500 fewer HDDs (gas-weighted) than the 6 year average, or about 89% of the average. This year, the continental US is already 96 HDDs behind last year through Nov 14. The forecast calls for some improvement over the next week or so.

Here is how 2016 fell behind last year:

Tuesday, November 15, 2016

Short Term Weather Forecast Still Shows Warmth

CPC forecasts show heating demand approaching normal seasonal levels in about 7 days.

Western Canada Stores More Natural Gas, Exports Less in November

Strong AECO Hub pricing this month is pushing more gas into storage, and less across the US border. High Canadian storage levels throughout the summer have been elevating exports, but that dynamic stalled at the beginning of November. Last year, 15.8 BCF was injected on the TC NOVA System in October, while 7.8 BCF was withdrawn this year. But as the chart shows, injections resumed on Nov 2 of this year, and have spiked to about 1 BCF per day over the last three days.

Texas Power Market Shows Impact of Renewables

The Demand and Energy Report just released by ERCOT for October shows that renewables are making a major difference in that sizable market. Long the leader in wind generation capacity, Texas is not slowing down much in the build out of additional resources, and now solar PV is beginning to appear on the radar.

It is impossible not to notice that wind power generated 46% as much power as natural gas did in October. Despite the claim that wind and natural gas are a perfect pairing, due to wind's intermittent variability, the reality is that it isn't a marriage of equals. Gas must accept the leftovers, and the larger the wind footprint, the more stable is the aggregate power output, reducing the call on gas fired generators.

Here is the graphical picture of the ERCOT 2015 vs 2016 generation mix as of October:

Monday, November 14, 2016

Western US Hydro Power Exceeding NOV 2015 by 3 GW

Better precipitation in the West this autumn has elevated stream flow in California and Wash/Oregon over the last month. This should prove temporary, but it has a large current impact on power generation.

A few strong early storms, and a late start to winter, is moving more water down the Columbia River dam system. Average hydro output in November is up 2GW over last year through the 13th of November. That surplus should diminish going forward, as normal rainfall and the beginning of snowpack begin to reduce the excess stream flow.

A few strong early storms, and a late start to winter, is moving more water down the Columbia River dam system. Average hydro output in November is up 2GW over last year through the 13th of November. That surplus should diminish going forward, as normal rainfall and the beginning of snowpack begin to reduce the excess stream flow.

Nuclear Power Fleet Recovering from Maintenance Faster Than 2015

The US nuclear power reactor fleet is completing its seasonal maintenance/refueling schedule sooner than it did in 2015, which is reducing demand for natural gas fired electricity generation by nearly 2 BCFD at present.

Friday, November 11, 2016

Haynesville Shale Rig Count Implies Production Increase Imminent

Haynesville Shale rig counts have been creeping upward since Q1 of this year, with horizontals hitting 20 this week. 70% of those rigs are working on the Louisiana side of the play, with 6 at work in DeSoto and 4 in Red River Parish. DeSoto Parish currently accounts for about 50% of the gas output from the Louisiana side, or about 1.6 of 3.2 BCFD that Louisiana contributes.

On the Texas side, the original HVS counties of Harrison and Panola are no longer leading development, with Rusk and San Augustine each deploying 2 rigs now, of the 6 at work in Texas.

Texas Oil and Gas Drilling and Completion Report Shows Increase in Drilling Permits

The Texas Railroad Commission Monthly Drilling, Completion and Plugging Summaries showed a third month of increasing permit activity in October, though reported well completions remained at a depressed level. The recent increase in rig counts should translate into rising completions by year end (though completions are often reported late).

Thursday, November 10, 2016

Warm Forecasts Compound Natural Gas Woes

Natural gas inventories rose by 54 BCF as reported by the EIA today. This brings inventories to record levels, with one more injection yet to come before storage begins declining. The short range weather forecast portends more pain for gas prices before the hope of a normal winter could bring meaningful demand.

Today's injection is on par with last year's +55, though weather was much warmer this year. It marks the fourth week that inventories have failed to shed excess levels, after six months of weekly reductions in the storage surplus.

US Oil Production Spikes 163K Barrels Per Day in One Week

Lower 48 crude oil production rose from 8.012 to 8.175 million barrels per day last week. This is the fourth increase in a row, and indicates that the rising rig count, or an increase in DUC well completions, is reversing the declining production trend. Output now sits 480K BOPD below this time last year, and 1 million barrels per day below the peak in June 2015.

Wednesday, November 9, 2016

Pemex Oil and Gas Production Continues Multi-Year Decline in September

Pemex reported another substantial decline in gas and liquids production in September, with Crude down 1.4% and Natural Gas down 1.2% on the month.

Crude output fell 31 KBOPD from August to a new low of 2.11 million barrels per day, a 7% annual decline.

Natural Gas fell 67 MMCFD on the month, a 13.2% annual decline. A 0.85 BCFD decline in 1 year is substantially more than the total increase in NG exports to Mexico from the U.S. The largest gas production declines were in onshore, non-associated production. Crude declines were more evenly spread across grades and regions, though the northern region was unchanged, an area of low production to begin with.

Subscribe to:

Posts (Atom)