The Eagle Ford is one area where production has been growing quickly. But rigs have been steadily moving from the dry to the wet side of the play. Transportation constraints are a factor as well, and gas has a harder time getting out of the basin. Here is what the Texas RRC reports for gross production by month from the major counties in the play. Note that Liquids = Crude and Condensate, not NGLs. NGLs are still in the gas stream at the well head:

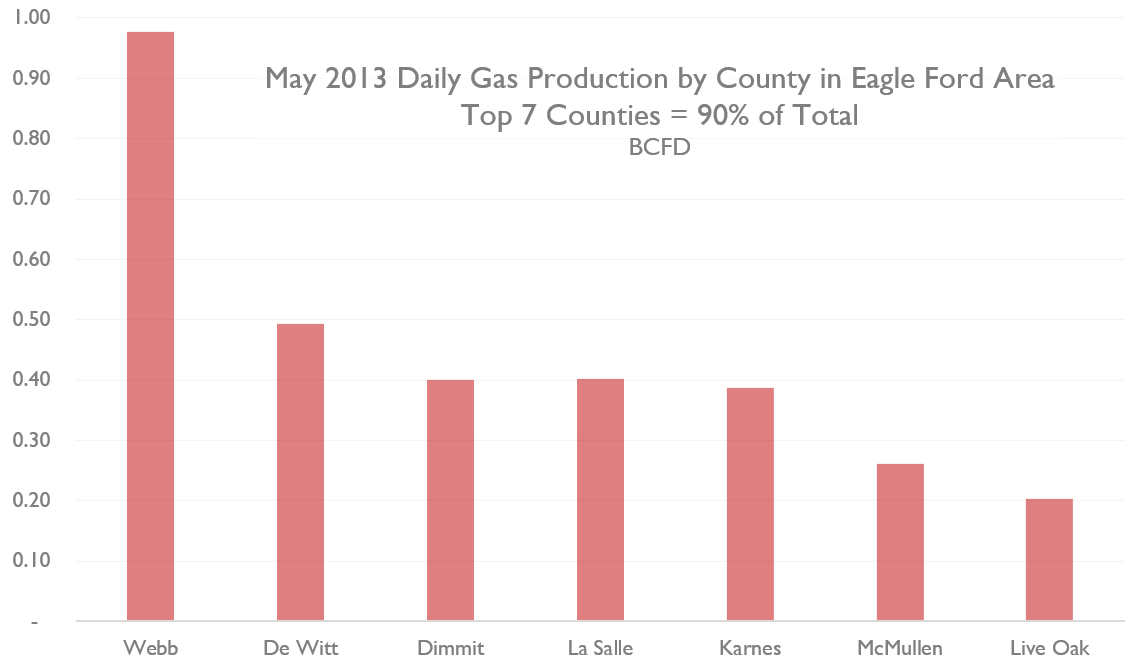

90% of the natural gas is produced in 7 counties, with Webb producing the lion's share. At May 2013, here is the relative contribution:

The drilling results from the wetter regions have wide ranging GORs, but the coveted acreage can produce over 90% liquids, so it is unclear whether associated gas will make a major contribution going forward.

Dry gas reserves on the other hand are ample, so a price signal and pipeline should bring the rigs back quickly. Drill times in the EF are much faster than Haynesville or Marcellus, so a small rig count can be deceiving. The best in class wells are drilling around 10 days to TD now, and that will undoubtedly improve. A crude model of potential production looks a little like this:

37 Rigs @ 2 wells per month x 5 BCF per well = 370 BCF developed per month. At that constant drilling rate, production would asymptotically approach 12 BCFD (370 BCF per month / 30 days). So that's still impressive. The Haynesville has about the same rig count, but wells take about twice as long to drill, and have a similar EUR of 5-6 BCF.