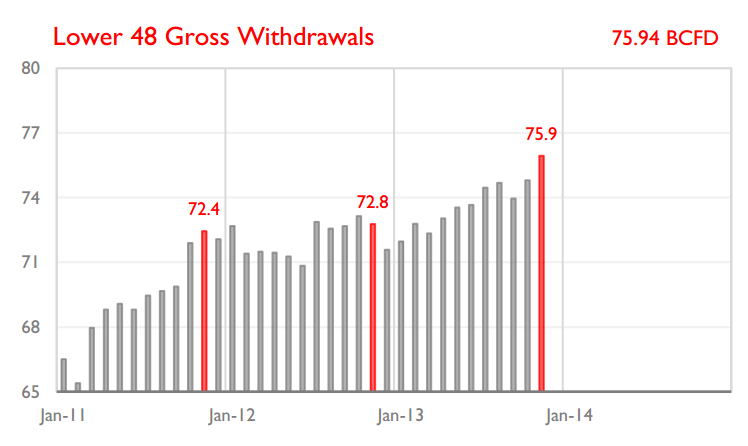

Low gas rig counts and inventories appear to be driving a rally in near month gas prices as cold weather lingers. But the forward strip beyond 2014 is not moving up. Much has been made of the fact that virtually every producing basin is in decline, excepting the Marcellus/Utica and the Eagle Ford. But consider another angle on the same data: The net gas production growth in the last three years was the result of swelling tight gas performance offset in part by steep declines in other major legacy basins. Those steep declines are not going to continue because they can't.

The overall massive increase in gas production:

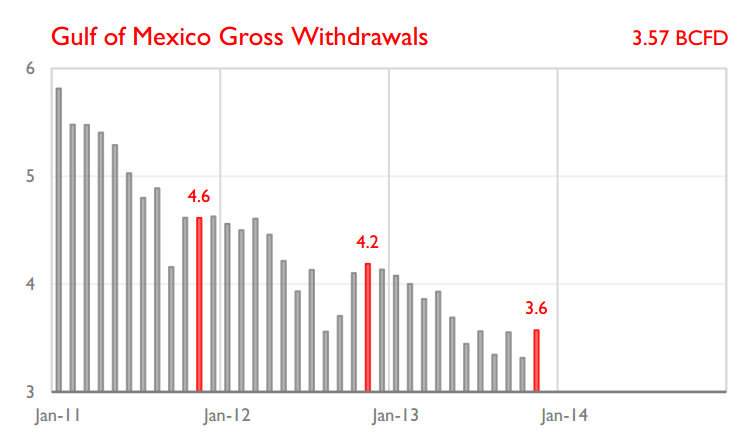

Meanwhile, output from the Gulf of Mexico, Louisiana, and Wyoming have combined for a loss of about 6.6 BCFD from their respective peaks in that same time frame.

Louisiana has been the largest contributor to the decline, with the Haynesville almost cut in half from its peak output. As these basins stabilize (or even continue their declines at the same %), there will be far fewer legacy production losses offsetting further growth in the top shale basins. And there is the potential that the Gulf could return to a production growth path, as long lead times for projects that were interrupted by the Macondo incident are completed.

If the current rally in gas prices begins to infect the forward strip, marginal shale plays like the Haynesville and even the Barnett will likely see some recovery in activity, with so few rigs working now.

This is not to suggest that production is guaranteed to skyrocket, but it does indicate that the sources of production growth could still drive national production increases without sustaining the steep output trajectories we have seen in the early years of development.