Despite a cold January this year, and accompanying high electricity loads, natural gas lost out to coal fired generation. Gas has shown significant price elasticity, especially during the spring shoulder season, where YOY pricing has risen drastically from 2012 to 2014. And this in the face of what has clearly been a structural shift toward gas fired new capacity and coal retirements.

Few new coal retirements are scheduled in 2014, but a substantial volume will shut down as MATS is implemented through 2015. Some of the largest new capacity additions are coming in Ohio and Florida.

Here are the gas vs coal market share patterns in both those states recently. Quite a difference in coal dependency. Gas already dominates in Florida, while Ohio is coal dependent as expected. Florida has seen coal retake significant market share of fossil fuel powered electricity generation.

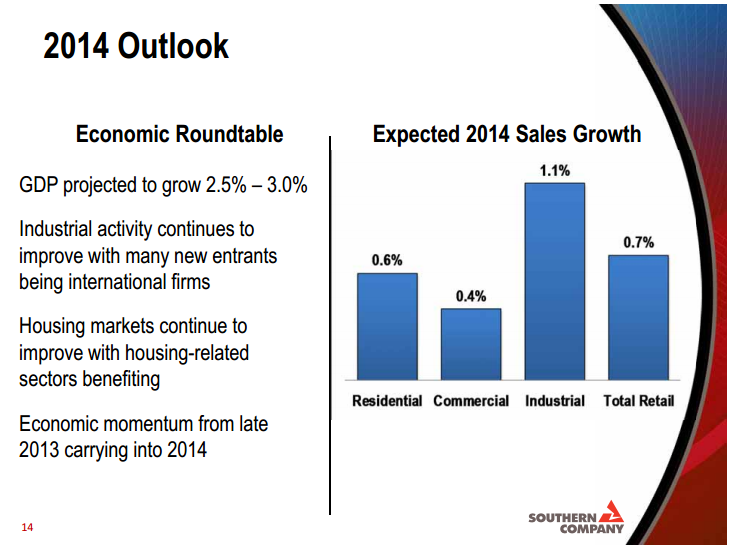

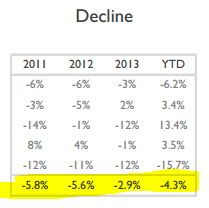

Another data point from the south too, Southern Co reports these operating stats for Q4 2013, showing a definite decline in natgas in favor of coal:

However, they are (somewhat) optimistic about 2014 growth: